Introduction

The COVID-19 pandemic has taken Australia and the world by surprise. Coming after severe drought conditions in eastern Australia, concerns have been raised about Australian food security. These concerns are understandable, but misplaced.

Australia does not have a food security problem

Despite temporary shortages of some food items in supermarkets caused by an unexpected surge in demand, Australia does not have a food security problem.

[expand all]

What is food security?

Food security refers to the physical availability of food, and to whether people have the resources and opportunity to gain reliable access to it.

The 1996 World Food Summit defined food security as the situation “when all people, at all times, have physical and economic access to sufficient, safe and nutritious food to meet their dietary needs and food preferences for an active and healthy life” (FAO 1996).

More technically, the four pillars of food security are availability, access, utilization and stability of supply (FAO 2006).

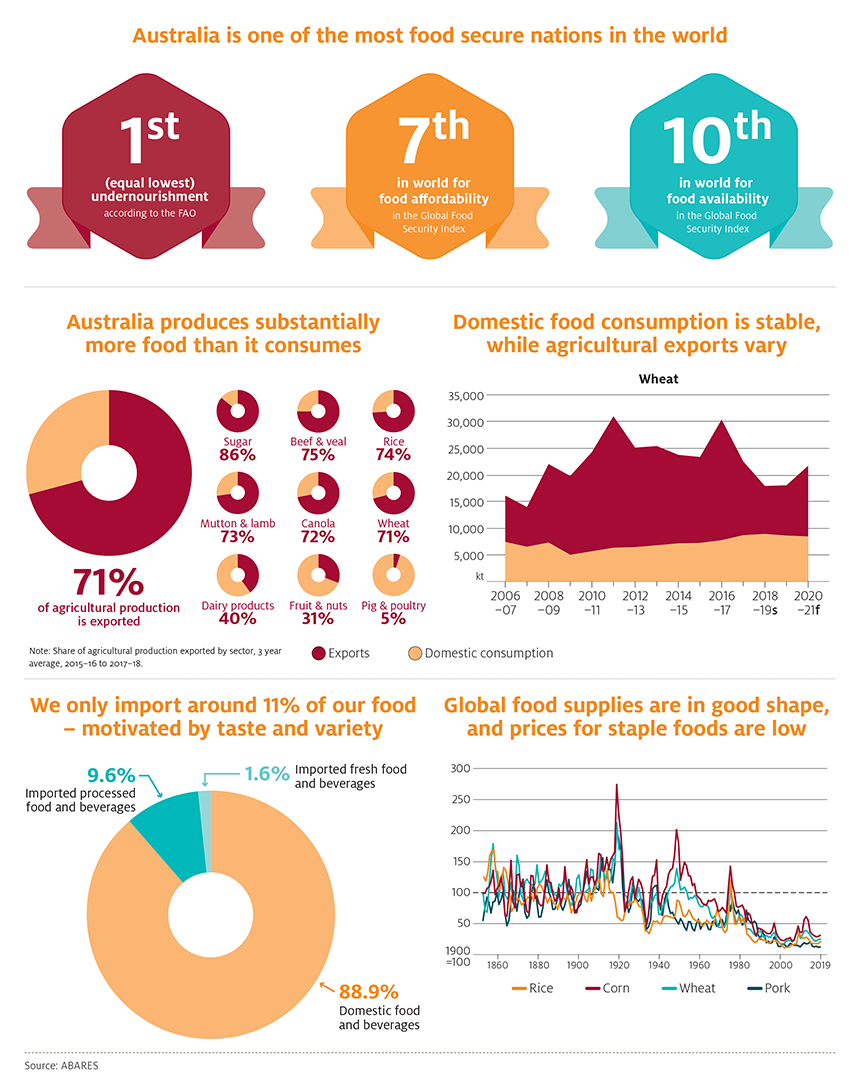

Australia ranks among the most food secure nations in the world, alongside Canada, Germany, and France (EIU 2020). Australia is a high income country, ranking 12th in the world for per capita income, and the vast majority of Australians can purchase basic foodstuffs that provide adequate nutrition. Australians benefit from being able to choose from an enormous and growing number of food products sourced from all over the world at affordable prices (Martin and Laborde 2018), and can access diverse and high-quality foods regardless of seasonal conditions or changes in world prices. We are in the top 10 countries in the world for affordability and availability, and have the world’s equal lowest level of undernourishment (FAO 2019).

Australia also plays a part in the food security of other countries. International trade – including Australian food exports – supports food security in other countries through providing physical access to food, lowering prices, and making food more economically accessible. Australia also contributes to food security in other countries through agricultural research, development assistance, and the transfer of Australian agronomic knowledge and expertise (D’Occhio 2011).

Australia is one of the most food secure nations in the world, with access to a wide variety of healthy and nutritious foods.

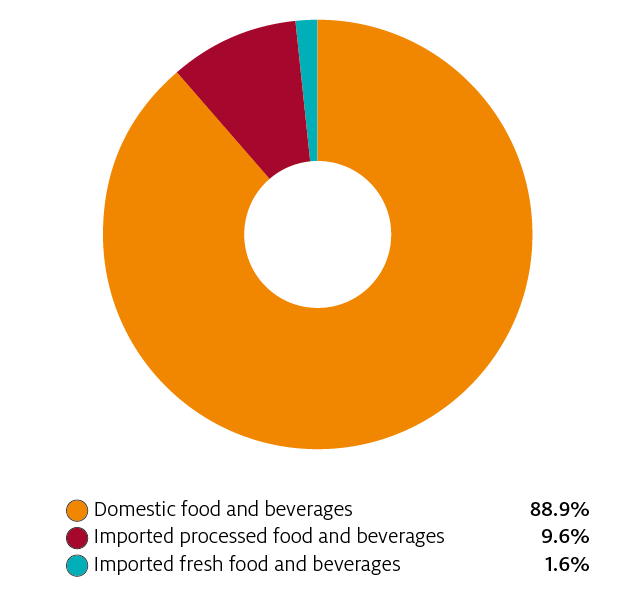

Australia is one of the most food secure countries in the world, for several reasons. Australia produces much more food than it consumes, exporting around 70% of agricultural production.

We do not produce everything we like to eat however, and imports account for around 11% of food consumption by value. These imports provide access to manufactured food and beverages, different varieties of some items, and out of season fresh produce.

Disruptions to international supply chains by COVID-19 (or other causes) are unlikely, but could result in temporary shortages of some imported products, restricting consumer choices in a similar way to how a cyclone might disrupt the domestic supply of bananas for a time.

The seasonal outlook for the autumn of 2020 is positive, providing the basis of a recovery in Australian crop production and allowing for rebuilding of sheep flocks and cattle herds.

Empty supermarket shelves reflect an unexpected surge in demand (as consumers stockpile food), taking supply chains by surprise

Uncertainties around the impacts of COVID-19 triggered a sudden increase in purchasing by consumers of a range of items, resulting in disruption to stocks of some basic food items in supermarkets.

This disruption is temporary and not an indication of food shortages. Rather, it is a result of logistics taking time to adapt to the large unexpected surge in purchasing.

The purchasing surge already appears to be abating, and supply chains are adapting. Panic buying and stockpiling of staple goods, such as rice and pasta, is likely to be balanced over time by a reduction in future purchases.

We only import around 10% of our food – motivated by taste and variety

The vast majority of food and beverages consumed in Australia are sourced from domestic production. Australian households spend just 11 cents in the dollar on imported products as a share of total food and beverage expenditure (excluding takeaway and restaurant meals), as shown in Figure 1.

These imports play an important role in meeting consumer preferences for taste and variety.

The majority of food and beverage imports are processed products (including frozen vegetables, seafood products, and beverages), along with small amounts of out-of-season fresh produce. Potential disruptions to these imports would be unlikely to have any impact on Australian food security – in terms of ensuring a sufficient supply of healthy and nutritious food – although higher prices or limited availability of specific products may disappoint or inconvenience some consumers.

Notes: Imports of processed and fresh (primary) food and beverages, as a share of total food and beverage consumption including tobacco and alcohol by value, three year average 2016–17 to 2018–19.

Source: ABS 2019, 2020a.

Australia produces substantially more food than it consumes

Australia typically exports about 70% of agricultural output in years with average or favourable seasonal conditions. Australian agricultural exports were worth more than $48 billion dollars in 2018–19, accounting for 13% of Australia’s overall merchandise export earnings (ABARES 2020; ABS 2020a).

The export orientation and level of trade exposure varies across different agricultural sectors, as shown in Figure 2. Some of our largest sectors, such as beef and wheat, are heavily export focused. Other sectors like horticulture, pork and poultry sell most of their production into the domestic market, with an emphasis on supply of fresh produce. Australia is a net importer of a small number of food commodities to supplement domestic consumption and meet consumer preferences for variety, mainly seafood, processed pig meat products and out-of-season fruit and vegetables.

Australia also imports some agricultural inputs such as soybean meal, which is mixed with Australian grain to produce poultry feed. This allows the domestic industry to specialise and control input costs while taking advantage of higher income generating opportunities in national and international markets.

Australia produces more rice than it consumes in most years, supported by improved varieties that are adapted to Australian conditions. However, consumer preferences for specific varieties of rice make it more profitable to export some of our rice and import other varieties. Drought conditions occasionally result in net imports because of low domestic production – as occurred in 2019–20 and previously after the 2006–07 drought. This reflects that in dry years it is more profitable to use the limited water available in other industries, particularly to maintain permanent plantings.

Notes: Share of agricultural production exported by sector, 3 year average, 2015–16 to 2017–18

Source: ABARES, following method outlined in Cameron (2017).

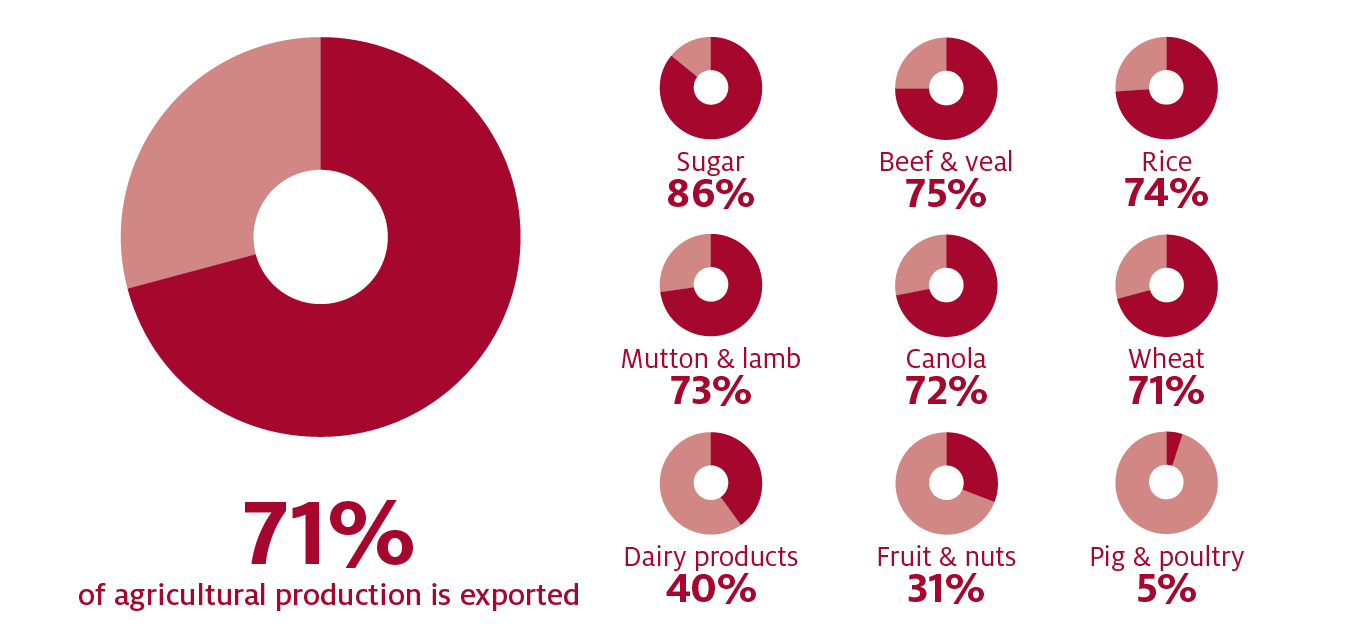

Australia’s agricultural exports act as shock absorber, keeping domestic food supply stable

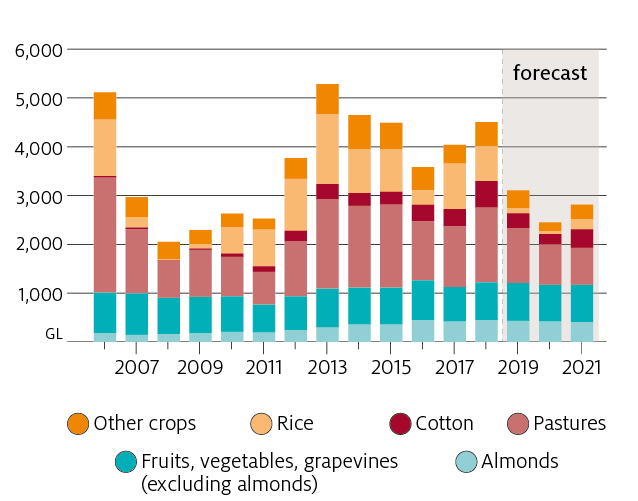

Australia is a net food exporter, including in severe drought years, producing more food than required for domestic consumption (see Figure 3).

This results in domestic consumption remaining stable while exports vary, absorbing the ups and downs in annual production associated with Australia’s variable climate and seasonal conditions.

Notes: Domestic consumption and export estimates for wheat, beef, rice, fruit and nuts, 2006–07 to 2020–21. Fruit and nuts covers table grapes, apples, pears, oranges, mandarins, peaches, mangoes, bananas, almonds and macadamias. s estimate. f forecast.

Source: ABARES 2020.

The outlook for rainfall is positive, and production is expected to recover

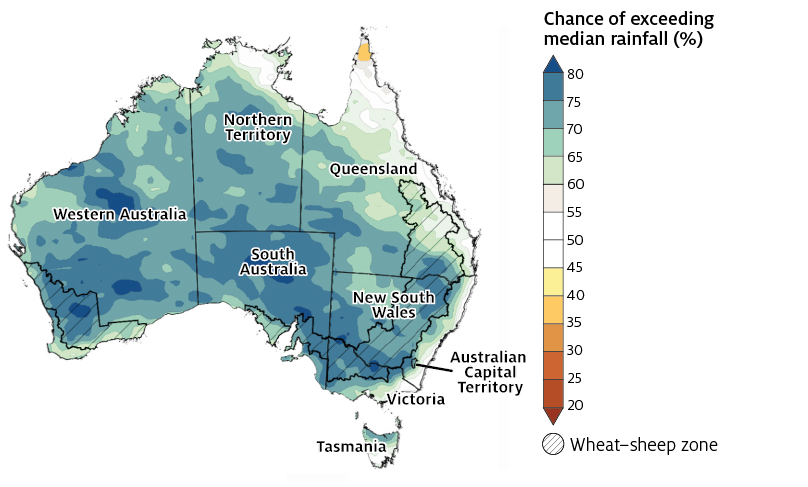

After a hot and dry 2019 and widespread drought conditions in NSW and Queensland, above-average rainfall during the first three months of 2020 has improved production conditions in some key agricultural regions across eastern Australia. The latest Bureau of Meteorology seasonal forecast suggests that rainfall in coming months is likely to be higher than average across most of Australia (see Figure 4).

There is a high chance that rainfall during autumn and winter will be sufficient to sustain crop and pasture production in many areas where soil moisture is close to average (or higher) for this time of year following an early autumn break. In New South Wales, for example, there is a 75% chance of receiving between 25 mm in the north-west and 200mm in the east of the state between April and June.

Recent rain and a positive seasonal forecast provide the potential for the best agricultural production in several years. While current prospects for winter crops are good, more rain is required for this to be realised.

ABARES is forecasting that grain production is likely to return to close to average levels, with a significant chance of higher production given the good start to the winter cropping season. For livestock producers, better seasonal conditions provide an opportunity to rebuild herds and flocks following a relatively long period of destocking. It will take some time to rebuild cattle and sheep numbers from current historically low levels, and water prices in the Murray Darling Basin (MDB) are expected to remain relatively high.

Notes: Map shows chance of exceeding median rainfall for the period May to July 2020, showing above average rainfall is likely or very likely across all inland areas of Australia, including the wheat–sheep zone.

Source: Bureau of Meteorology (issued 9 April 2020)

Irrigated agriculture is important for many reasons, but domestic rice plays a modest role in Australian food security

Irrigated crops account for about 30% of the value of agricultural production and over 90% of agricultural water use. Irrigated crops include export-oriented fruit, nuts and rice production, and largely domestically oriented vegetables and other horticulture. These industries contribute to export earnings, provide fresh food for domestic consumption, and play an important role in supporting regional communities and employment. The MDB accounted for 41% of the gross value of Australian production of fruit, nuts, vegetables and other horticulture, and 44% of Australian dairy production in 2017–18.

Recent pressures on food supply chains due to the COVID-19 outbreak have prompted calls for governments to intervene in MDB water markets to boost production of certain commodities, such as rice.

Irrigation water is actively traded in the MDB by farmers, and Australian water markets are considered to be among the most advanced in the world, adding to the profitability and resilience of irrigation agriculture. Water markets allow farmers to shift water between alternative uses, so that water is used in the most productive and profitable way, in both wet and dry years. This helps manage the economic impacts of Australia’s highly variable water supplies.

In practice, water markets result in water being used for high-value crops even in dry years – including vegetables and perennial plantings (including fruit and nuts). But water use by other crops, including rice and pastures is quite variable with significant decreases in water use in dry years when water prices are high.

Notes: Water use for fruits, nuts and vegetables does not vary significantly with total water availability. Water use by export-oriented perennial plantings of almonds has increased over time due to their relative profitability, leading to an increase in the area planted. Water use by rice, dairy and other irrigated pastures vary significantly with water availability and price.

Source: ABARES, Australian Bureau of Statistics.

The latest Bureau of Meteorology seasonal outlook (discussed above) suggests water availability is likely to improve from drought-affected levels. This would begin to refill water storages in the Basin and elsewhere, lifting the volume and value of irrigated output. ABARES forecasts that a return to average seasonal conditions would see rice production increase from 54,000 tonnes in 2019–20 to levels of about 180,000 tonnes in 2020–21. Based on past experience, in a normal year about 74% of this production would be exported.

But it will take consecutive years of good rainfall and water recharge to lower water prices. As a result, ABARES expects water prices to remain relatively high in the coming year (Westwood et al 2020).

If seasonal conditions do not improve, markets will allocate water to its highest value economic use, resulting in lower domestic rice production and continued imports of rice to meet domestic consumption.

All of the water in the MDB is allocated, and so government intervention to provide additional water to a particular sector or producer would need to take water from some other use, such as reserves held to ensure future town water supply or environmental outcomes, or water that would have been used more profitably in another sector (reducing the gross value of irrigated production).

Global food supplies and food access are in good shape

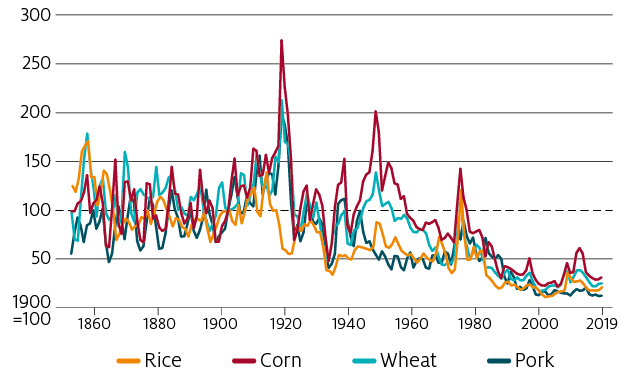

Global food supplies and access have improved dramatically over the last 70 years, driven by increased physical productivity and crop yields – particularly as a result of the Green Revolution. This has seen a long run decline in real commodity prices and production costs (adjusted for inflation) from 1950, as increasing agricultural supply has outpaced increases in demand driven by population growth and rising average incomes.

Global microeconomic reforms and lower trade barriers since the 1980s have added to these improvements in agricultural productivity and food accessibility (Jacks 2019, Martin and Ivanic 2016, Martin and Laborde 2018). However, despite this substantial global progress, many low and medium-income countries continue to struggle with food insecurity, poverty, and malnutrition (Pingali 2012).

Notes: Real prices, adjusted to remove the effects of inflation. Index 1900 prices = 100.

Source: Jacks 2019

Global grains stocks are currently abundant.

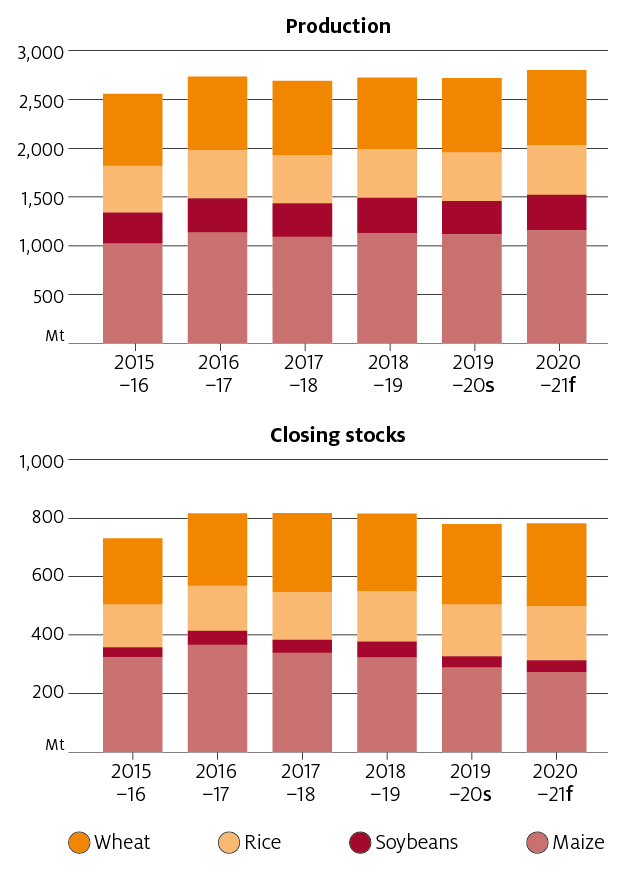

The International Grains Council is forecasting that world wheat, rice, maize (corn), and soybean production will all reach record levels in 2020–21 (Figure 7), with stocks of wheat and rice also increasing, adding to already large inventories.

As a result, world cereal prices are expected to remain low for the next few years.

Notes. Total grain production is projected to increase 84 million tonnes (Mt) (4%) from 2018–19 to 2020–21. Stocks of wheat and rice are projected to increase by 18 Mt and 12 Mt respectively, while stocks of soybeans and maize (or corn)—used for food, feed grains for livestock, and ethanol production—are projected to fall by 15 Mt and 49 Mt respectively, resulting in a projected reduction in total carryover stocks of 34 Mt (–4%).s estimate. f forecast.

Source: IGC 2020

These low global prices and ample stocks of food grains provide a valuable backstop for countries who rely on imports to ensure low cost supply of essential foods.

The COVID-19 pandemic poses a range of risks to food security in some countries, however, notwithstanding the solid foundation provided by current food stocks. These risks are of particular concern in low-income countries, with lower purchasing power and more vulnerable supply chains, and may be exacerbated by other factors – such as crowded or insecure housing and living conditions.

Trade is crucial to food security, affordability, and regional stability

International trade is crucial to global food security, as well as to Australia’s national income and economic performance. Trade lowers food prices for consumers in importing countries. Participation in global agricultural markets also reduces price volatility and the potential for food price spikes (particularly in droughts or other periods of low-domestic production) because weather and other supply risks are shared across global production and exports, resulting in more stable prices and supply volumes (Anderson 2014, OECD 2017).

These trade-related improvements in food security also contribute to improved social stability and resilience, particularly in countries with higher levels of poverty or more variable growing conditions.

Trade restrictions – such as import quotas or tariffs – can increase domestic food production in good years, but also increase domestic food prices and food price volatility, reducing economic access for urban and poor rural households (who are more likely to be net food buyers).

Trade restrictions also make countries more vulnerable to extreme events and poor local seasonal conditions. They thus generally reduce national food security (as shown by Anderson 2014, OECD 2017), despite improving food self-sufficiency in average and good years.

In the current pandemic, concerns over food security have caused some major exporters of staple products to once again consider restricting exports. Such measures applied during the 2007 and 2008 food price crisis significantly increasing world prices and amplifying the impact on poverty and food insecurity (Martin and Ivanic 2016). Although such actions would have little impact on Australia (as a high-income net food exporter), they would be likely to increase food insecurity and have negative impacts on consumers in low and medium-income nations.

Global supply chains and migrant labour provide important inputs to Australian agriculture – and will require careful attention and management

Australian agriculture relies on international markets and supply chains for a range of inputs.

While substantial prolonged disruptions seem unlikely, it will be important for business and government to monitor potential vulnerabilities and actively manage associated risks.

Domestic and international freight and logistics

Domestic transport is an essential supporting service for agriculture. Road and rail transport are likely to continue to operate with minimal disruptions, with arrangements in place to safely exempt freight services from restrictions designed to limit the community spread of COVID-19. Trucks appear to be moving freely between regions, including interstate, and will continue to do so. This will facilitate the distribution of inputs to farms, outputs (including livestock and produce) from farms to processing facilities, and food from processing facilities to retail outlets.

In terms of exports, there has been some disruption to airfreight and the availability of shipping containers.

Airfreight is important for commodities such as seafood, horticulture and meat exports but accounts for less than 3% of the value of Australia’s exports.

A substantial share of international airfreight travels on passenger flights, which have been heavily affected by international travel bans. As a result, demand for air freight capacity is now exceeding supply, causing costs to rise sharply. The Government has announced $110 million in financial assistance to help high-value, air-freighted agricultural and seafood products reach key overseas markets. Implementation of this assistance will also seek opportunities for return flights to carry Personal Protective Equipment (PPE) and medical supplies to respond to COVID-19.

Some concerns have been raised regarding the availability of shipping containers, particularly refrigerated containers, with a risk that below-average inbound arrivals could limit the number of containers available for outbound exports. Data on shipping arrivals indicate that after a normal seasonal slowdown in February, March arrivals have remained low, potentially restricting the supply of containers.

With production and trade recovering in China, these potential shortages may be resolved in the short-to-medium term. Prices for containerised freight have started to fall globally, after initial increases in January, providing a basis for cautious optimism.

Fertiliser and agricultural chemicals

There have not yet been any significant disruptions to the availability of fertilisers or chemicals. Chemical supply companies report some short term COVID-19 related disruption to international manufacture and distribution of chemicals (such as glyphosate) have been largely resolved. While strict health and safety provisions are already in place for the manufacture and distribution of these chemicals, the risk of further disruptions is difficult to judge.

If significant supply chain disruptions do occur, farm productivity and profitability could be reduced if farmers need to switch to more costly or less-effective alternative chemicals, or agronomic strategies for managing pests and diseases.

Inputs to food processing

Food processing and packing rely on a range of inputs, particularly packaging, which may be subject to supply chain disruptions. For these mostly manufactured products, it is likely that alternative supply pathways can be found if disruptions appear imminent. However, establishing these alternative pathways will generally involve additional effort and may also involve higher costs, which could erode profit margins and increase consumer prices.

Labour in horticulture, farming and food processing

Labour is an essential input to agricultural production.

Social isolation is a normal and easily achieved characteristic of Australia’s broadacre cropping and grazing industries, where farming often involves small numbers of family employees operating on large areas of land. Exemptions on movement restrictions for shearers and machinery contractors will facilitate business continuity in these industries.

In contrast, horticultural industries are labour intensive and rely on a relatively unskilled and itinerant workforce brought in for short periods from outside local areas, often involving backpackers from overseas. This is particularly the case for harvesting of fruit and vegetables. These factors make these industries vulnerable to being disrupted by COVID-19 restrictions on international and domestic travel, and accommodation requirements.

Meat processing facilities in some regions face similar issues, with migrant workers accounting for a significant proportion of the workforce.

On 4 April 2020, the Government announced temporary visa arrangements aimed at ensuring a sufficient supply of labour for agricultural industries during the COVID-19 crisis. These include that agricultural workers from overseas will be able to extend their visas; agricultural workers will be able to travel providing they fulfil requirements aimed at stopping the transmission of the virus between regions; and agricultural workers will be able to stay with one employer for longer.

Australian consumers can be confident in our food security

Australia is one of the most food secure countries in the world, with ample supplies of safe, healthy food. The vast majority of our food is produced here in Australia, and domestic production more than meets our needs even during drought years.

Australia imports just over 10% of domestically consumed food and beverages, to meet consumer preferences for taste and variety. It is unlikely – but possible – that COVID-19 could disrupt these supply chains temporarily, resulting in inconvenience for some consumers. This would not threaten the food security of most Australians.

Australian agricultural producers rely on global supply chains and imported inputs. Shortages or disruptions to these inputs could impact on productivity and profitability, and it will be important for business and government to actively monitor and manage emerging risks.

References

ABARES 2020, Agricultural commodities: March quarter 2020, Australian Bureau of Agricultural and Resource Economics and Sciences, Canberra.

ABS 2020a, International trade in goods and services, Australia, Feb 2020, cat. no. 5368.0, Australian Bureau of Statistics, Canberra.

ABS 2020b, Consumer price index, Australia, December 2019, cat. no. 6401.0, Australian Bureau of Statistics, Canberra.

ABS 2019, Australian system of national accounts, 2018-19, cat. no. 5204.0, Australian Bureau of Statistics, Canberra.

ABS 2017, Australian national accounts: input–output tables, 2016–17, cat. no. 5209.0.55.001, Australian Bureau of Statistics, Canberra.

Anderson, K, 2014, The intersection of trade policy, price volatility, and food security, Annual Review of Resource Economics, 6:1, pp. 513-532.

Cameron, A 2017, ‘Share of agricultural production exported’, in Agricultural commodities: December quarter 2017, Australian Bureau of Agricultural and Resource Economics and Sciences, Canberra.

D’Occhio M, 2011, ‘A food secure world – challenging choices for our north’, in The Crawford Fund Highlights Newsletter, 2011.

EIU 2020, Global food security index, Economist Intelligence Unit, London.

FAO 1996, Rome declaration on food security and world food summit plan of action, World Food Summit 13-17 November, Rome, Italy.

—— 2006, Food security, FAO Policy Brief, Issue 2, June, Food and Agriculture Organization of the United Nations, Rome.

—— 2019, The state of food security and nutrition in the world, Food and Agriculture Organization of the United Nations, Rome.

—— 2017, Suite of food security indicators: domestic food price volatility (index) – value, Food and Agriculture Organization of the United Nations, Rome, accessed 6 April 2020.

Jacks, D, 2019, From boom to bust: a typology of real commodity prices in the long run, Cliometrica 13:2, pp. 202-220.

Martin, W and Ivanic, M, 2016, ‘Food price changes, price insulation, and their impacts on global and domestic poverty’, in M. Kalkuhl, J. von Braun and

M. Torero (eds) Food price volatility and its implications for food security and policy, Springer International Publishing: 101-113.

Martin, W and Laborde, D, 2018, The free flow of goods and food security and nutrition, Chapter 3 in Global food policy report: 2018, International Food Policy Research Institute, pp. 20-29, Washington DC

OECD 2017, Building food security and managing risk in Southeast Asia, OECD Publishing, Organization for Economic Cooperation and Development, Paris.

Pingali, P, 2012, Green revolution: impacts, limits, and the path ahead, PNAS 109:31, pp. 12302-12308. https://doi.org/10.1073/pnas.0912953109.

Westwood, T, Whittle, L, and Gupta, M, 2020, ABARES water market outlook: March 2020, Australian Bureau of Agricultural and Resource Economics and Sciences, Canberra.

Errata

In figure 2, rice exports as a percent of total production has been amended from 52% to 74% after conversion weights from paddy rice to milled rice were corrected. Updated on 1 May 2020.

Download the report

ABARES Insights: Analysis of Australian food security and the COVID-19 pandemic – PDF [0.69 MB]